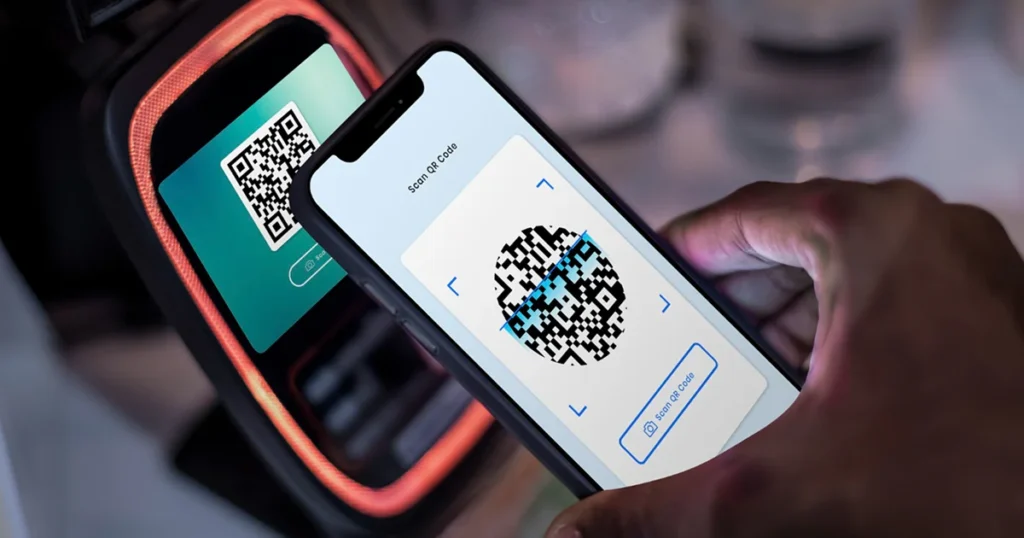

Contactless payments have exploded in India after UPI made digital transactions mainstream. In 2026, users expect to pay by simply tapping phones or smartwatches at stores. Two technologies power this convenience – NFC and BLE. NFC enables tap-to-pay like credit cards while BLE connects devices over short distances for payments. Building contactless payment apps requires understanding how these technologies work and Indian payment ecosystem regulations. Security is critical as one mistake can expose user financial data. The Indian contactless payment market is growing 40-50% annually as more merchants install compatible terminals. This blog explains BLE and NFC technologies in simple language and guides building secure contactless payment apps for the Indian market.

Understanding NFC Technology

NFC or Near Field Communication enables communication between devices placed very close together.

NFC uses radio waves communicating when devices are within 4 centimeters of each other. One device creates a small electromagnetic field that powers the other device. No battery needed in payment cards or tags receiving power from phone’s NFC chip.

Payment apps store encrypted card information in phone’s secure element. When tapping phone at payment terminal, NFC transmits encrypted payment data. Transaction completes in under a second without internet connection required.

NFC is extremely secure due to very short range preventing interception from distance. Works offline without mobile data enabling payments anywhere. International standard means compatibility with payment terminals worldwide including India.

Understanding BLE Technology

BLE or Bluetooth Low Energy enables slightly longer-range communication between devices.

BLE works up to 10 meters distance compared to NFC’s 4 centimeters. Requires Bluetooth enabled on both devices unlike NFC’s automatic activation. Uses minimal battery power enabling always-on functionality.

BLE enables payments at kiosks, vending machines, and parking meters from short distance. Users select items on their phone and confirm payment without physically tapping terminal. Merchants can push payment requests to nearby customer phones.

Longer range is convenient for certain payment scenarios like drive-through or parking. However, longer range also means more security considerations than NFC. Requires active pairing adding slight friction compared to NFC tap-and-go.

Building Secure Payment Apps

Security is paramount when building apps handling financial transactions.

Never store actual card numbers in apps or transmit them during payments. Use tokenization converting card details into meaningless tokens. Even if tokens are intercepted, they cannot be used elsewhere.

Store payment credentials in phone’s secure element, a separate chip isolated from main operating system. Secure element prevents malware from accessing sensitive payment data. Both Apple Pay and Google Pay use secure elements.

Encrypt all payment data from app to payment gateway using industry-standard protocols. Encryption prevents man-in-the-middle attacks intercepting transaction data. Use only proven encryption methods, never create custom security.

React Native: Building Dynamic Apps with JavaScript

Never store actual card numbers in apps or transmit them during payments. Use tokenization converting card details into meaningless tokens. Even if tokens are intercepted, they cannot be used elsewhere.

Store payment credentials in phone’s secure element, a separate chip isolated from main operating system. Secure element prevents malware from accessing sensitive payment data. Both Apple Pay and Google Pay use secure elements.

Encrypt all payment data from app to payment gateway using industry-standard protocols. Encryption prevents man-in-the-middle attacks intercepting transaction data. Use only proven encryption methods, never create custom security.

Indian Payment Ecosystem Requirements

Reserve Bank of India regulates digital payments with strict security requirements. Apps must comply with two-factor authentication for transactions above certain amounts. NPCI certification is required for apps integrating with UPI and RuPay.

Integrate UPI enabling contactless payments directly from bank accounts. UPI with NFC enables tap-to-pay using bank balance instead of cards. This combination is uniquely popular in India compared to card-focused international markets.

Indian users prefer having multiple payment options including cards, UPI, and wallets. Apps supporting Visa, Mastercard, RuPay, and UPI see 60-80% higher adoption. Flexibility matters more in India than single-method simplicity.

Technical Implementation Steps

Check if user’s phone has NFC hardware before enabling NFC features. Guide users to enable NFC in phone settings if disabled. Gracefully degrade to alternative payment methods for phones without NFC.

Integrate with payment gateways like Razorpay, PayU, or Paytm supporting contactless. Gateways handle complex tokenization and certification requirements. Direct integration with banks requires extensive compliance work.

Conduct penetration testing identifying potential vulnerabilities before launch. Test against common attacks like replay attacks and man-in-the-middle. Security audits by third parties provide independent validation.

Conclusion

BLE and NFC technologies enable convenient, secure contactless payments that Indian users increasingly prefer. NFC provides ultra-secure tap-to-pay for terminals while BLE enables slightly longer-range scenarios. Building secure payment apps requires tokenization, secure element integration, and end-to-end encryption. Indian market requires RBI compliance, NPCI certification, and UPI integration alongside card support. Technical implementation involves capability checking, payment gateway integration, and rigorous security testing. User experience matters greatly with clear confirmations, graceful failure handling, and offline support. The Indian contactless payment market growing 40-50% annually presents significant opportunities.

Frequently Asked Questions

Do all Indian smartphones support NFC for contactless payments?

Approximately 60-70% of smartphones in India now include NFC chips. Mid-range and premium phones almost always have NFC while budget phones may lack it. BLE is available on virtually all smartphones as alternative.

How much does it cost to build a contactless payment app?

Basic contactless payment app costs approximately4-7 lakhs including security implementations. Full-featured apps with multiple payment methods and compliance range 25-50 lakhs. Security and compliance represent significant portion of costs.

What security certifications are required in India?

RBI compliance and NPCI certification are mandatory for payment apps. PCI DSS certification required for apps handling card data. Security audits by recognized firms provide additional credibility.

Can small merchants afford contactless payment terminals?

NFC terminals now available for approximately 2,000-5,000 rupees making them affordable for small merchants. UPI QR codes remain free alternative not requiring hardware. Contactless terminals becoming economically viable for most businesses.

How long does contactless payment app development take?

Basic contactless payment integration takes approximately 3-5 months including testing. Complete app with full feature set requires 6-10 months. Security testing and certification add 2-3 months to timeline.